ECB Interest Tate Decision and Impact on GOLD

ECB interest rate decision

After Fed Chair Jerome Powell’s hawkish speech on the FOMC interest rate decision last week, which hammered the price of gold down, European Central Bank governor Christine Lagarde blew the same trumpet on Thursday. At first glance, the interest rate decision by the ECB did not bring about any changes, but in your speech you made some long overdue admissions, to which the price of gold also reacted with discounts.

She stated that “the risks to the inflation outlook are pointing to the upside” , while so far the country has been reassured and the high inflation rates have been sold as only “temporary”. She added that the board was “unanimously concerned” about the high inflation figures . Lagarde also noted that inflation is “approaching the ECB’s target” but added that it will not raise rates until net asset purchases have ended . While she said in December that rate hikes in 2022 were “very unlikely ,” she didn’t repeat that statement this time .

The ECB therefore expects prices to continue to rise and is groping its way towards interest rate hikes and an end to bond purchases. If you no longer print money that devalues the purchasing power of the euro, there is no reason to keep gold in your portfolio as a hedge against inflation, at least that is the opinion of many investors. For this reason, short-term speculators reflexively sold gold last week and new buyers held back, which put the price under pressure for a short time.

In view of the historically strong increase in European consumer prices in January of 5.1 percent, interest rate hikes are long overdue. As soon as the ECB ends its bond purchases, the market will try to compensate for inflation and the bond markets will continue to slide until a fair market level has been reached or the ECB comes on the floor as a buyer again. Particularly due to the highly indebted Southern European countries, the European Central Bank will not leave the rise in interest rates to the market, as this could quickly become a new stress test for the European Union.

1

Prices in the European Union rose by 5.1% in January. Nevertheless, the dollar rose after Lagarde no longer ruled out a rate hike in 2022

Therefore, one will have to intervene early with new bond purchases and thus the printing of money out of thin air in order to prevent interest rates from rising too quickly. As soon as the ECB dares to even hint at this move, the demand for gold as a hedge against further inflation will explode and its price will rise sharply.

In the short term, we must therefore expect a continued trendless phase and, in the worst case, brief setbacks on the gold market. However, since it is already clear that central banks have maneuvered themselves into a corner, they will be back to the printing presses sooner rather than later, so these latest declines present buying opportunities. The correction potential seems to be limited, although the catalysts for price increases are currently missing. However, a military conflict in Ukraine would be a black swan that could change the situation overnight and initiate the next upward impulse in gold prices.

2

Gold market volatility is declining — a breakout to the upside or down could be imminent

Good labor market data at the end of the week weigh on the price of gold

The ADP jobs report for January was a surprise surprise last week, losing 301k jobs instead of the expected 200k increase. The market consensus for the US government’s monthly jobs report was correspondingly low at 150k. But, as is so often the case, the ADP numbers were not a good indicator as the US Labor Exchange surprised traders on Friday afternoon with 467k new nonfarm payrolls in January.However, this increase is likely to be primarily due to a seasonal adjustment of the statistics. In addition, the figures for the two previous months have also been revised upwards. In December instead of 199 thousand, 510 thousand new jobs were created and in November instead of 249 thousand as many as 647 thousand.

Wages rose by 0.7% m/m ( +5.7% YOY ) with only a 0.5% increase expected. As these jobs numbers support the Fed ‘s plans, 10-year Treasury yields rose to 1.92% and 2-year Treasury yields to 1.3%, making March’s rate hike safe. Some are already suspecting a surprise hike of 50 basis points, which could hit the gold price again in the short term at the next central bank meeting in March.

3

Surprisingly good jobs data have increased the likelihood of further rate hikes

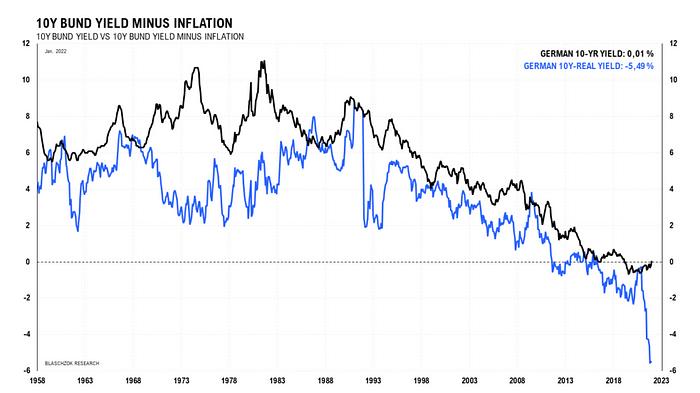

Overall, the market’s reaction to the supposedly restrictive monetary policy by selling gold is a mistake. The amount of money that has been flushed into the system over the last two years has had a relatively small impact on consumer prices so far. It may take another two to three years before the money ultimately also fully affects consumer prices via higher energy and raw material prices. An increase in key interest rates will not change this depreciation in the purchasing power of the euro. Currently, the ten-year federal bonds bring an annual loss of 5.5% and even an increase in the key interest rate to a normal market level of 10% would not change the coming devaluation of the euro .

The bluff of fighting inflation

While it’s true that rising interest rates limit new borrowing in a free market, it’s a common misconception that raising interest rates can help the central bank combat the inflationary potential it created by printing money. It is clever media propaganda and the constant repetition of this false statement that the ECB would raise interest rates to fight inflation. In fact, it’s exactly the opposite. Since they created inflation by printing money out of thin air, the market is now demanding inflation compensation in the form of higher interest rates, and the central bank ultimately has to give in to this demand and raise interest rates. This has absolutely nothing to do with fighting inflation.

10-year Bunds are currently losing an inflation-adjusted 5.5% per year

The only possible way to fight or reverse the further increase in consumer prices would be to extract the liquidity that the ECB has pumped into the system over the past two years. It had doubled its total assets to 9.6 trillion euros, while debts have been mounting worldwide. The US national debt passed the $30 trillion barrier for the first time last week! The decade after the housing and credit crises of 2008 has shown that neither the FED nor the ECB has ever significantly withdrawn the liquidity they created out of thin air and pumped into the monetary system.

So those investors who are currently selling gold believing the price can’t go any higher are dead wrong. On the contrary, consumer prices will continue to rise and interest rates with them, while the real economy will slide into recession, to which central banks will sooner or later have to react by printing money again. The real negative interest rates will bring the holders of government bonds large real losses and the stock markets will continue to come under pressure. Western economies are caught in the stagflation that will be with us through the end of the decade. Therefore, use every setback to further build up your gold holdings!

Gold Technical Analysis: Was Gold Price Manipulated Ahead of Fed Meeting?

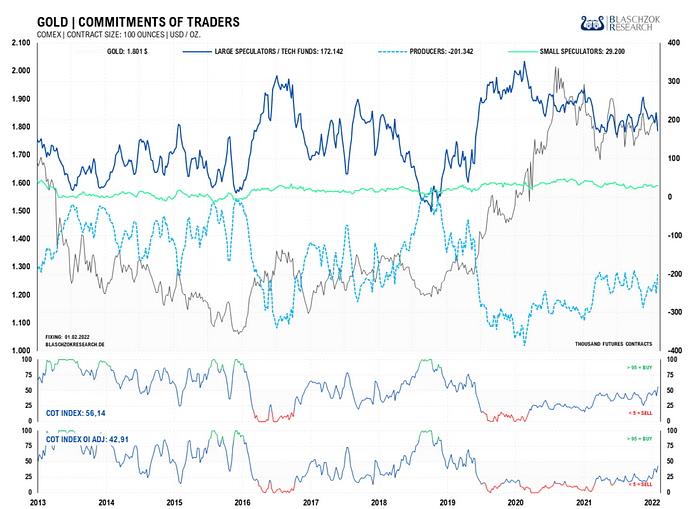

Derivatives market: COT report from February 4th, 2022

The latest COT report was published on Friday at 9:30 p.m. by the US futures market regulator with the key date of February 1st. Premium subscribers received a flash update with analyzes on gold, silver , platinum and palladium before the close of trading . This new report had it all and points to a small storm that could sweep over the gold and silver markets again in the short term.

The price of gold fell by $46 on the previous week, while speculators’ aggregate positioning was reduced by 48 thousand contracts, which in itself already shows weakness on the previous week and the previous month. In addition to this weakness, however, there is also a coverage of the BIG4 in the amount of 4 days of world production. Without this coverage by the BIG4, gold would have fallen even lower after last week’s Fed meeting. So the manipulators used the post-Fed meeting panic selling to scale back their naked short position.

In the week leading up to the Fed’s interest rate decision, gold prices were stalled with 8 days of world production after gold prices surged above $1,835 to prevent a further rise. After Jerome Powell’s hawkish speech, the weakness was used to partially close the short position with a profit. This is a typical pattern when further corrections are imminent, which we now have to assume.

Over the longer term, the overall short position in the BIG4 is relatively small, which is more indicative of an impending bottom of a correction or bottoming. However, a pullback to $1,680 would be possible again, but we currently do not see any more correction potential.

The prospect of rising interest rates and a planned reduction in the central bank’s balance sheet are further weighing on the price of gold. It seems as if they are now taking the opportunity to knock on the price.

5

Gold futures data remains in neutral territory

In the last two weeks a typical manipulation over the futures market could be observed

The markets believe the central bankers that they would be able to raise interest rates and withdraw liquidity from the market again. In this deflationary environment gold would be unnecessary as a hedge against inflation. Therefore, new buyers are currently holding back, some are selling their holdings and speculators are trying to profit from falling prices. The manipulation of the futures market is an indication that this correction will be enforced if necessary in order to demonstrate the strength of fiat currencies and to discourage investors and speculators from this stretching torture.

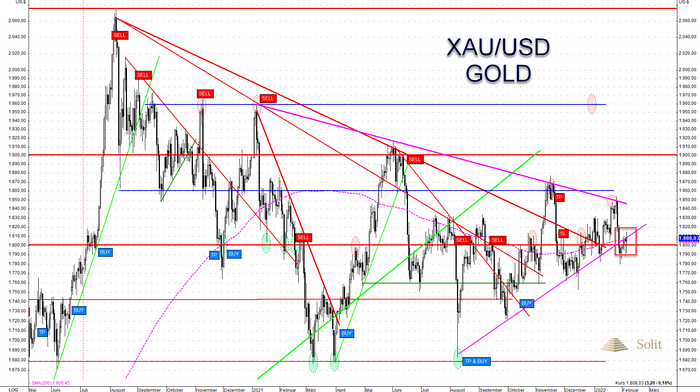

Technically, the support around $1,800 remains significant and is being hotly contested by bulls and bears. The fact that the gold price is still above this is only due to the renewed weakness of the US dollar after the ECB meeting — if the dollar strengthens again, the price of gold should fall and the bulls will throw in the towel.

There is a risk in trading that gold could slip further to $1,725 or $1,680. Short-term traders are therefore shorting below $1,800 while medium-term investors stand on the sidelines and wait. There is a rather low probability of gold struggling back above $1,855 in the near term due to new exogenous factors. In this case, short-term traders cautiously go long on it in stages, but the risk-reward ratio (CRV) for doing so is not good.

Bulls and bears are fighting at the key support at $1,800

The daily chart shows that the price of gold is not only struggling with the support at $1,800, but also with a short-term uptrend. If this cross-support breaks, a pullback to $1,680 is very likely.

The daily chart also clearly shows the medium-term downward trend, on which the price of gold was recently slowed down. Only with an increase above the last historical high and thus above the downward trend above 1,855 US dollars would a medium-term procyclical buy signal arise. Those who want to be on the safe side with buying should wait until this downtrend has been broken or buy anti-cyclically in the $1,680 area.

If the uptrend breaks, the correction is likely to continue

The long-term downtrend for gold in euros was already broken at 1,480 euros in May, which provided a long-term buy signal. For more than half a year, the gold price in euros consolidated at this new support at 1,480 euros. A downtrend formed on the upside and the price increasingly wedged.

There was another pro-cyclical buy signal after the gold price had overcome the blue downward trend in mid-October with closing prices above EUR 1,540. The price then rose to almost 1,660 euros. This resistance was reached simultaneously with the resistance at $1,870.

In the last week of trading, the price of gold in euros fell out of the short-term uptrend with a stronger euro after ECB President Christine Lagarde’s speech, generating a short-term sell-signal. In the worst case, we see a correction to around EUR 1,520 — above that, the bullish starting position remains intact. The stop loss for this short trade must be placed at 1,608 euros.

The correction potential for gold in euros seems limited, but there are currently few potential catalysts that could drive the price. A military conflict in Ukraine could immediately change monetary policy and thus the outlook for gold prices, but until then we must continue to expect a trendless phase and possibly a final correction.

As long as the gold price is above EUR 1,520, the bullish setup will remain intact

Watch The Detailed Analysis on my channel here